This insideAI News technology guide co-sponsored by Dell Technologies and AMD, insideAI News Guide to Big Data for Finance, provides direction for enterprise thought leaders on ways of leveraging big data technologies in support of analytics proficiencies designed to work more independently and effectively across a few distinct areas in today’s financial service institutions (FSI) climate.

Introduction

Across industries, data continues to grow as an extremely valuable resource. This is especially true in the financial services sector. “Financial services” is a broad term that encompasses commercial banks, investment houses and insurance companies. This highly competitive sector has been largely dominated by global conglomerates, with a diverse range of smaller companies. Financial services institutions (FSIs) have always been a substantial consumer of information technology, usually ahead of other industries. For the past several years, FSIs have continued that trend by leveraging big data analytics and artificial intelligence (AI) to enable new opportunities and deliver benefits to customers and employees alike.

About a decade ago, big data became an emergent trend driving investments in enterprise analytics, and correspondingly, analytic excellence is central to much needed innovation in today’s financial services marketplace. Business analytics applied to capital management, regulatory compliance, corporate performance, trade execution, security, fraud management, and other instrumental disciplines is the principal innovation platform to improving strategic decision making. But now, the financial services sector is witnessing an era of digital disruption and innovation, driven by the following macro trends:

- Increased regulation: In the aftermath of the 2008 financial crisis, financial service institutions (FSIs) have become subject to greatly increased regulations for controlling risk and understanding exposure. Risk controls previously done weekly or nightly are now done several times per day— sometimes in near real time. Compliance with regulations, such as the Fundamental Review of Trading Book (FRTB) and the Comprehensive Capital Analysis and Review (CCAR), involve simulating a huge number of parallel market scenarios and over large portfolios simultaneously. This requires computing power that stretches the limits of traditional computing.

- High consumer expectations: Tech savvy consumers are increasingly seeking financial services that are faster, cheaper, more personalized and easier to access.

- New, more agile players in the market: A growing field of financial technology (fintech) companies is shaking up traditional business models, eroding market share and undercutting margins for incumbents.

- Emerging technologies: Breakthrough technologies such as artificial intelligence (AI), including deep learning and machine learning, are allowing early adopters—both fintechs and established companies—to gain massive differentiation and will produce significant disruption over the coming years.

With mounting regulations, customer expectations and disruptors around every corner, FSIs will need to embrace digital transformation to prosper and stay competitive. FSIs recognize the power of technology to shape their futures, and CIOs now drive a large part of the company strategy. This new generation of FSI IT leaders are seeking to securely and rapidly enhance their digital capabilities to reduce costs, grow share and provide better customer experiences.

The goal for this Guide is to provide direction for enterprise thought leaders on ways of leveraging big `data technologies in support of analytics proficiencies designed to work more independently and effectively across a few distinct areas in today’s FSI climate:

- Retail Banking

- Regulatory and Compliance

- Algorithmic Trading

- Security Considerations

Retail Banking

Thanks in large part to the availability of data and the movement from in-person to online banking, today’s banking institutions look very different than those of just a decade ago. As the scale of data is overwhelming traditional systems, banks must adapt to new technologies to unlock the power of their data.

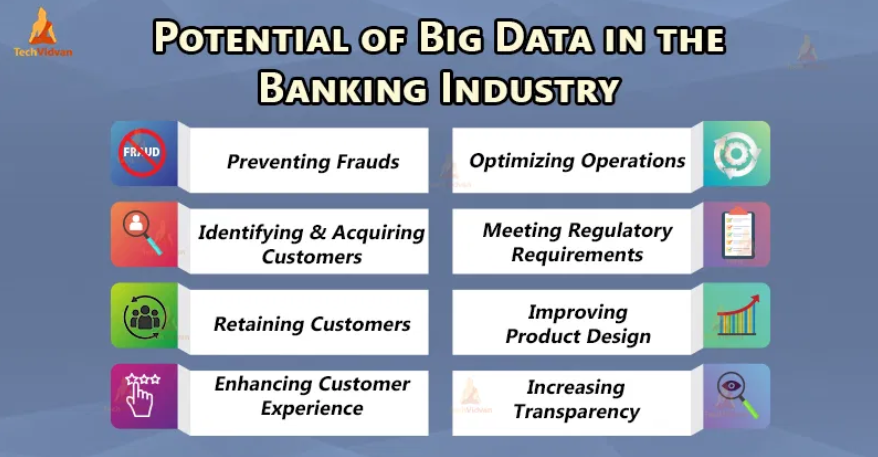

Banks have long been considered innovators when using data analytics to tackle numerous business challenges such as risk management, fraud detection and price discovery. Yet today, the volume of data is much bigger and more diverse than ever before.

At the same time, regulatory demands for banks have become much more stringent and the increased level of historical storage requirements have meant that banks must keep data for longer periods of time. This complexity has necessitated new approaches and technologies leading to big data infrastructure.

There are a number of motivating factors for engaging big data technology in support of retail banking:

- The availability and scale of data is extraordinary and requires a new technology mindset.

- A significant transition from in-person to online banking resulting from the ease and affordability of executing financial transactions.

- A distinct need to collect and analyze this information in order to accurately assess risk and market trends.

- The availability of new data sources such as data from social media, blogs and other news feeds offer significant new opportunities. As with all online markets, banking is competitive and banks are interested in using any opportunity, identified through data, to cross sell and upsell customers.

Coupled with the above motivations, there are a number of potential application areas for big data in retail banking:

- Since banks weigh the risk of opening new accounts versus the opportunity to hold deposits, big data can screen new account applications for risk of default. In addition, big data can identify high- risk borrowers for auto loans.

- Maximizing customer touch points leading to better customer service and churn detection and avoidance.

- Cross-sell/up-sell using recommender systems.

- Monetize anonymous banking data in secondary markets.

Solving the challenging problem of customer churn is one good example of how big data can make a real difference for retail banking. With credit card transactions, loyalty programs, and many other customer touch points, banks possess far more data about customers than any other industry, but in spite of all the data, customer-centric companies like banks are often unable to deliver effective personalized service. The main reason is the low level of customer intelligence.

The world is increasingly interconnected, instrumented and intelligent and in this new world the volume, velocity, and variety of data being collected is unprecedented. As the amount of data created about a consumer is growing, the percentage of data that banks can process is going down fast. Based on their engagement with popular consumer destinations like Amazon or Yelp, customers have expectations about similar experiences from the banking applications. Without deep know-how about their customers, banks may not be able to meet these expectations.

The result? Lost revenue opportunities, low coupon redemption rates, lower share of customer’s wallet and lost competitive agility. In a nutshell, not being able to gain insights from the goldmine of data means banks are allowing their competitors to identify critical business trends and act on those before they can, ultimately losing business. In summary, in order to advance the level of customer intelligence banks must:

- Leverage big data to get a 360-degree view of each customer.

- Drive revenues with one-to-one targeting and personalized offers in real-time.

- Reduce business risk by leveraging predictive analytics for detecting fraud.

- Achieve greater customer loyalty with personalized retention offers.

- Employ the power of big data without worrying about complexities and steep learning curves.

There are many quality software tools allowing banking institutions to reap the benefits of big data. For example, many FSIs use Splunk to collect information as an industry leading big data platform designed to integrate information of all types into easily deployed visualizations.

HOW DELL TECHNOLOGIES HELPS

Dell Technologies and Splunk partner to make adopting Splunk simpler, by engineering a portfolio of purpose built solutions with non disruptive scalability and performance optimized for Splunk workloads. Together, Dell Technologies and Splunk enable you to harness the power of machine data analytics with simplified deployment and scalability.

In summary, the banking market and consumers who utilize finance products generate an enormous amount of data on a daily basis. While each activity is a single data point, multiple pieces of information creates a larger picture that can be used to recognize patterns in customer behavior, purchasing choices and other key insights. AI and data analytics have changed the way all this information is processed, making it possible to identify trends and patterns which can then be used to inform business decisions, in real time, at scale. Leveraging technologies like Splunk and Dell Technologies, help FSIs achieve this desired outcome.

Over the next few weeks we will explore these topics:

- Introduction, Retail Banking

- Regulatory and Compliance, Algorithmic Trading

- Security Considerations, Conclusion, Next Steps with Dell Technologies and AMD

Download the complete insideAI News Guide to Big Data for Finance courtesy of Dell Technologies and AMD.

Speak Your Mind